Home inspection payment options explained simply: the buyer pays the inspector directly, almost always before or at the time of the inspection. The national average cost runs $343–$500, though homes under 1,000 square feet can start near $200 and larger properties over 3,000 square feet can exceed $500. That fee is not a formality. 86% of inspections uncover issues that give buyers an average of $14,000 in negotiation leverage. Knowing your payment methods, timing, and bundling options before you schedule puts you in control from day one.

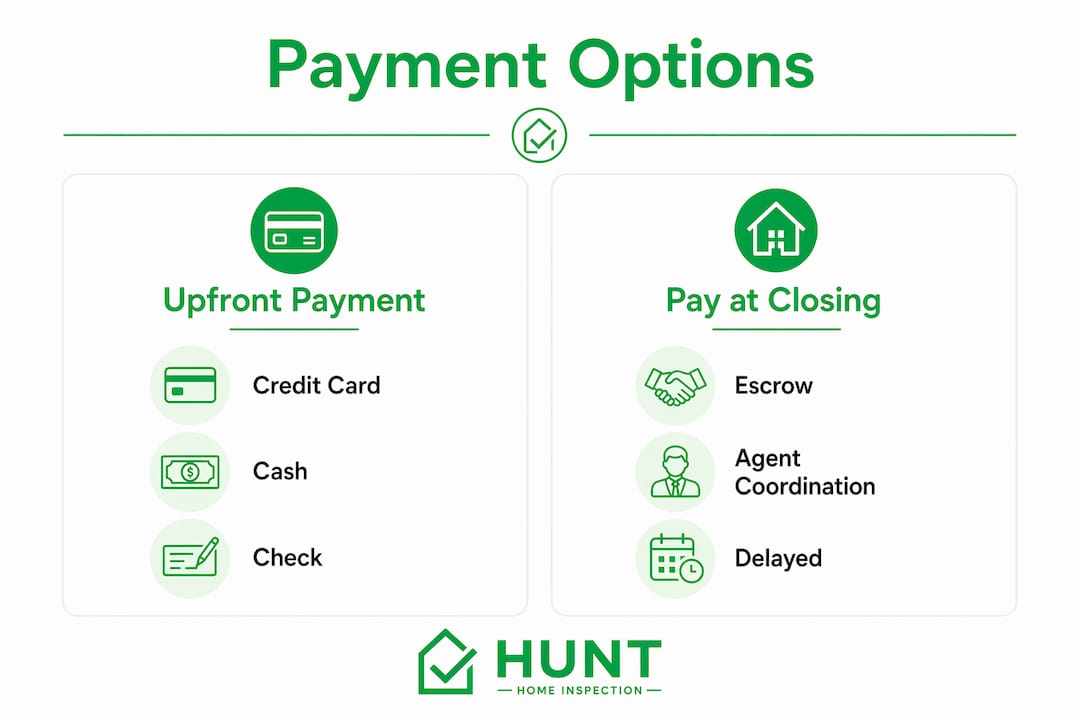

What payment methods do home inspectors accept?

Most home inspectors accept credit cards, debit cards, cash, and personal checks as standard payment methods for home inspections. Digital payment platforms like Zelle and ACH bank transfers are increasingly common, especially among independent inspectors who want to avoid card processing fees. Cash remains the simplest option and some inspectors prefer it for exactly that reason.

Card payments are convenient, but they come with a catch. Many inspection companies pass along a convenience fee of roughly 3% to cover processing costs. On a $400 inspection, that adds $12 to your total. It is a small amount, but worth knowing before you hand over your card.

Here is a quick breakdown of what to expect from each method:

- Credit or debit card: Widely accepted, instant, but may carry a 3% convenience fee

- Cash: No fees, preferred by some inspectors, requires exact change or ATM planning

- Personal check: Accepted by most inspectors, no fee, but requires a checkbook

- Zelle or ACH transfer: Fee-free digital options, increasingly offered by independent inspectors

- Pay-at-closing (escrow): A deferred option covered in the next section

Pro Tip: Ask about fees before you book. A quick phone call or email confirming accepted payment methods and any surcharges takes 60 seconds and prevents surprises on inspection day.

Always confirm payment terms when you schedule. Some inspectors require payment before they release the report, which is standard practice across the industry.

How does pay-at-closing work for home inspections?

Pay-at-closing is a deferred payment structure where your inspection fee gets rolled into your final closing costs instead of being paid on inspection day. It requires upfront coordination between you, your inspector, and your title or escrow company. Not every inspector offers this option, so you need to ask early in the process.

Here is how the process typically works:

- Confirm eligibility. Ask your inspector if they participate in pay-at-close arrangements before signing any agreement.

- Get written authorization. Your inspector, escrow officer, and real estate agent all need to agree in writing on the deferred payment terms.

- Provide a backup payment method. Most inspectors require a credit card on file in case the transaction falls through before closing.

- Review the closing disclosure. The inspection fee will appear as a line item. Verify the amount matches your original quote.

- Close on time. Delays in closing can complicate payment release, so stay in close contact with your escrow officer.

This option genuinely helps buyers who are managing tight cash flow during the contingency period. Earnest money, appraisal fees, and moving costs all hit at once. Deferring the inspection fee by even a few weeks can ease real pressure.

“Buyers often prefer pay-at-closing to manage out-of-pocket expenses, but must plan carefully to avoid last-minute issues.” — Strong Tower Inspections

There is one trade-off worth knowing. Pay-at-close payments often cannot be combined with coupons or seasonal promotions because the administrative overhead negates those savings. If your inspector is running a first-time buyer discount or a bundle special, paying upfront usually gets you the better deal.

Pro Tip: Loop in your real estate agent the moment you consider pay-at-closing. They have done this before and can flag any escrow company requirements specific to your state or transaction.

Bundled inspections vs. a la carte: which saves more?

A standard general inspection covers the structure, roof, electrical, plumbing, and HVAC. But many buyers also need specialty services like radon testing, sewer scope inspections, and termite evaluations. Paying for each one separately adds up fast.

Bundling specialty services with your general inspection saves 5–15% compared to booking each service individually. On a $600 total order, that is $30–$90 back in your pocket with zero extra scheduling effort.

| Service | A La Carte Estimate | Bundled Estimate | Typical Savings |

|---|---|---|---|

| General inspection | $400 | $400 | Baseline |

| Radon test | $150 | $120 | $30 |

| Sewer scope | $175 | $145 | $30 |

| Termite inspection | $100 | $85 | $15 |

| Total | $825 | $750 | ~$75 |

Bundles make the most financial sense when you already know you need multiple services. If you are buying an older home, a sewer scope is rarely optional. If you are in a region with high radon levels, like the Midwest or Mountain West, radon testing is a practical necessity.

New construction buyers get an additional benefit from bundling. Inspectors tracking a property across multiple build phases develop familiarity with the structure that reduces the risk of missed defects. Locking in one inspector for pre-drywall, framing, and final walkthrough inspections creates continuity that a la carte booking simply cannot replicate.

The downside of bundles is commitment. You are locking yourself into one inspector for all services. If your general inspector is not certified for radon or sewer scope work, a bundle offer from them is not worth taking.

How do you choose the right payment option?

Choosing the right payment approach comes down to three factors: your cash position right now, your timeline to closing, and the scope of inspections you need. Here is how to think through each one.

- Assess your cash position. If you have already stretched your savings on the down payment and earnest money, pay-at-closing may be the right call. If you have flexibility, paying upfront often unlocks discounts.

- Compare quotes on scope, not just price. Quotes vary widely based on add-ons like thermal imaging and radon. A $300 quote that excludes thermal imaging is not cheaper than a $375 quote that includes it.

- Plan your timing with your agent. Your agent knows the escrow company’s requirements and can tell you whether pay-at-closing is realistic for your transaction.

- Ask about bundle discounts upfront. Most inspectors do not advertise bundle pricing on their websites. A direct question during booking often reveals options that are not listed publicly.

- Keep every written quote. Written quotes and agreements are legally binding documents for scope and fees. If a dispute arises over what was included, your written quote is your protection.

One more thing: inspection fees are sunk costs. If your deal falls through after the inspection, you do not get that money back. That reality makes it even more important to choose an inspector whose report quality justifies the fee, not just one who charges the least.

Pro Tip: Review the full inspection cost breakdown before you book. Understanding what drives pricing helps you ask better questions and spot low-ball quotes that cut corners.

Key takeaways

The most effective approach to home inspection payments is to confirm your method, timing, and bundling options before you schedule, not after.

| Point | Details |

|---|---|

| Buyers pay upfront by default | Inspection fees average $343–$500 and are due at or before the inspection in most cases. |

| Card payments may cost more | A 3% convenience fee on card transactions adds to your total; ask before booking. |

| Pay-at-closing requires coordination | Deferred payment needs written agreement from your inspector, agent, and escrow company. |

| Bundles save 5–15% | Combining radon, sewer scope, and termite services with a general inspection cuts total cost. |

| Never choose by price alone | Compare scope and included services; the cheapest quote often excludes critical add-ons. |

What i have learned about paying for home inspections

I have seen buyers make the same mistake repeatedly: they treat the inspection fee as a cost to minimize rather than an investment to maximize. A $350 inspection that misses a $12,000 foundation problem is not a bargain. A $475 inspection that catches it and gives you negotiation leverage is one of the best financial decisions you will make in the entire transaction.

Pay-at-closing is genuinely useful, and I recommend it for buyers who are cash-strapped during the contingency window. But I always tell people to read the fine print. If your inspector is running a first-time buyer discount, paying upfront and taking the discount almost always beats deferring payment and losing it. Do the math before you decide.

Bundling is where I see the most overlooked savings. Most buyers do not ask about bundle pricing because they do not know to ask. One conversation at booking can save you $75 or more and eliminate the hassle of scheduling three separate appointments. For new construction buyers especially, bundling across build phases is not just a money-saver. It is a quality control strategy.

My honest advice: be transparent with everyone involved. Tell your agent early if you are considering pay-at-closing. Tell your inspector upfront if you need multiple specialty services. The more information flows between all parties, the smoother the payment process goes. The pre-purchase inspection benefits extend well beyond the report itself when you plan the payment side correctly.

— JOHN

Flexible inspection payments with Jhunthomeinspections

Jhunthomeinspections serves first-time buyers, veterans, and low-income families across the St. Louis Metro area and Southern Illinois with transparent, flexible payment options built around your budget. You can pay by credit card, debit card, cash, or digital transfer, and Jhunthomeinspections offers a pay-at-close option with no added fee to the buyer, making it one of the more buyer-friendly arrangements in the region.

Bundle pricing is available across specialty services including radon, sewer scope, and termite inspections, so you get consistent quality and real savings in one booking. Every report comes back within 24 hours, and the proprietary Create Request List™ tool keeps your agent and escrow company aligned from inspection day through closing. Explore the full range of inspection services and find the payment setup that works for your transaction.

FAQ

Who pays for a home inspection?

The buyer pays for the home inspection in the vast majority of transactions. Sellers occasionally offer inspection credits in competitive markets, but this is not standard practice.

What is the average cost of a home inspection?

The national average runs $343–$500 depending on property size and location. Homes under 1,000 square feet can start near $200, while larger properties over 3,000 square feet often exceed $500.

Can you pay for a home inspection at closing?

Yes, pay-at-closing is available through some inspectors and requires written coordination with your escrow or title company. Not all inspectors offer this option, and it may exclude promotional discounts.

Is it cheaper to bundle inspection services?

Bundling specialty services like radon, sewer scope, and termite inspections with a general inspection typically saves 5–15% compared to booking each service separately.

Are inspection fees refundable if the deal falls through?

Inspection fees are non-refundable sunk costs. If the transaction does not close, you do not recover the inspection fee, which makes choosing a thorough, qualified inspector even more important from the start.

Recent Comments