A veteran home inspection is an in-depth, buyer-directed evaluation of a home’s mechanical and structural condition, designed to protect you from hidden defects the VA appraisal does not cover. The VA appraisal is mandatory and protects the lender. The home inspection is optional but works entirely for you. Understanding veteran home inspection benefits explained clearly is the difference between a confident purchase and a costly surprise. Jhunthomeinspections works with veterans across the St. Louis Metro area and Southern Illinois to make sure that difference stays in your favor.

What are the core differences between a VA appraisal and a home inspection?

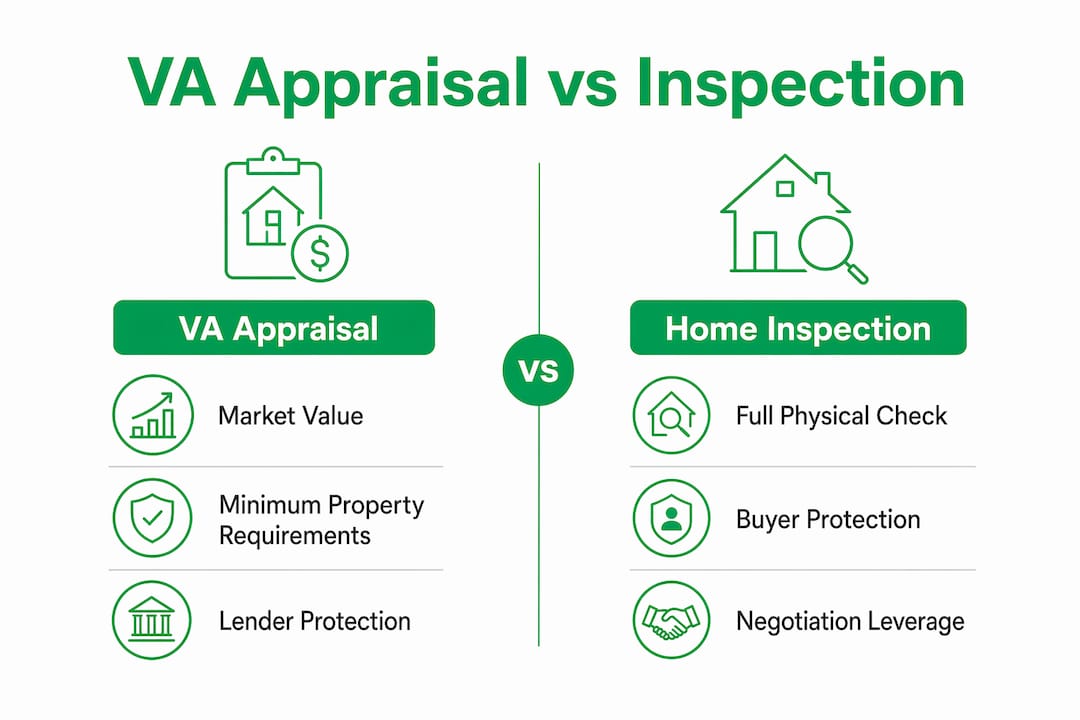

The VA appraisal and the home inspection serve completely different purposes. Confusing them is the most common and most expensive mistake veteran buyers make.

The VA appraisal focuses on two things: market value and Minimum Property Requirements (MPRs). MPRs are the VA’s baseline standards for safety, soundness, and sanitation. An appraiser confirms the home meets those standards and that the loan amount is justified. The appraisal report goes to the lender and the VA, not to you. It protects the lender’s investment, not yours.

The home inspection is a different tool entirely. A licensed inspector examines the roof, HVAC system, electrical panels, plumbing, foundation, and more. The inspection report belongs exclusively to you and gives you grounds to negotiate repairs, request seller credits, or cancel the deal.

What the VA appraiser does not check

VA appraisers follow strict guidelines that limit how deep they go. They never access crawl spaces or climb roofs. They conduct a visual walk-through, not a system-by-system test. That means a failing furnace, a leaking pipe behind a wall, or a deteriorated roof deck can pass an appraisal without a single flag.

A licensed inspector performs comprehensive system tests. The inspection typically takes 2–4 hours and covers everything the appraiser skips.

Pro Tip: Ask your inspector to walk through the property with you in person. You will learn more in two hours than you would reading the report alone.

Here is a side-by-side look at how the two evaluations compare:

| Feature | VA Appraisal | Home Inspection |

|---|---|---|

| Purpose | Market value + MPR compliance | Full physical condition evaluation |

| Ordered by | Lender | Buyer |

| Report goes to | Lender and VA | Buyer only |

| Roof access | No | Yes |

| Crawl space access | No | Yes |

| System testing | No | Yes |

| Typical cost | Varies by region | $350–$600 |

| Duration | Visual walk-through | 2–4 hours |

What are the key benefits of a home inspection for veterans using a VA loan?

The home inspection is the only tool in the transaction that works entirely for you. The VA appraisal protects the lender. The inspection protects your family and your finances.

Financial protection from surprise repairs

A failing HVAC system can cost $5,000 or more to replace. A deteriorated roof can run $8,000 or higher. Skipping the inspection to save $350–$600 often results in repair bills that dwarf the inspection fee many times over. The math is straightforward: one inspection fee versus thousands in unplanned repairs.

Negotiation leverage

Inspection findings give you real power at the negotiating table. You can present the report to the seller and request repairs before closing, ask for a price reduction to cover repair costs, or negotiate a credit at closing. Sellers respond to documented evidence. A written inspection report from a licensed professional carries far more weight than a verbal concern.

Safety assurance for your household

Veterans moving families into a new home need to know the property is safe. Inspectors identify issues like faulty wiring, carbon monoxide risks, mold indicators, and structural problems that pose direct safety threats. The VA’s MPRs set a floor, not a ceiling. An inspection goes well beyond that floor.

Long-term budgeting and planning

Inspection findings help you plan for future maintenance costs, not just immediate repairs. If the water heater is 12 years old or the roof has 5 years of life left, you can budget for those replacements before they become emergencies. This kind of forward planning is especially valuable for veterans transitioning from military housing to homeownership for the first time.

The right to walk away

Inspection contingencies in purchase contracts give you a legal option to cancel the deal based on inspection findings and recover your earnest money. This is one of the strongest protections a buyer has. If the inspection reveals severe structural damage or a compromised foundation, you can exit without penalty. That protection disappears if you waive the inspection.

Pro Tip: Never waive the inspection contingency to make your offer more competitive. The financial risk of buying a defective home far outweighs any short-term advantage in a bidding situation.

Veterans may also access home repair programs after purchase, including cash-out refinance options and disability housing grants, but those programs work best when you already know what repairs the home needs. An inspection gives you that knowledge before you close.

What costs and options should veterans consider when scheduling a home inspection?

A standard home inspection costs $350–$600 and takes 2–4 hours. That range shifts based on the home’s size, age, and location. Older homes and larger properties cost more because they take longer to inspect thoroughly. For a full breakdown of what drives pricing, the 2026 inspection pricing guide at Jhunthomeinspections covers the specifics.

Add-on inspections worth considering

The standard inspection covers the major systems, but some properties need additional testing. Common add-ons include:

- Termite inspection: Required by the VA in many regions. The VA termite inspection requirement is a separate evaluation from the standard inspection.

- Radon testing: Radon is a colorless, odorless gas linked to lung cancer. Testing is inexpensive and takes 48 hours.

- Sewer scope: A camera inspection of the sewer line. Older homes with clay or cast-iron pipes benefit most from this add-on.

- Private water testing: Required in some regions for homes on well water.

Each add-on typically costs $100–$300. Some regions require specific inspections by lender or local policy, even when the VA does not mandate them. Check with your lender early so you are not caught off guard.

Some lenders go further than the VA and mandate inspections as a condition of the loan, regardless of VA requirements. Confirm your lender’s policy before you schedule anything.

Scheduling the inspection before the appraisal gives you the most negotiating room. If you find problems and negotiate repairs, those repairs may need to be verified before the appraisal closes out. Getting the inspection done first keeps your timeline clean.

You can also get a free home valuation to pair with your inspection findings, giving you a complete picture of the property’s market position and physical condition before you commit.

How can veterans effectively use home inspection reports in their VA loan purchase process?

The inspection report is a working document, not just a record. Knowing how to use it separates veterans who protect their investment from those who absorb avoidable costs.

-

Review the report before the appraisal. Schedule your inspection as early as possible. Early scheduling gives you time to negotiate repairs or exit the deal before appraisal deadlines and non-refundable fees lock you in.

-

Prioritize findings by severity. Not every item in an inspection report is a dealbreaker. Focus on structural issues, safety hazards, and major system failures first. Cosmetic items can be addressed after closing.

-

Submit a formal repair request. Present the inspection report to the seller with a written list of requested repairs or credits. Use the report’s language and the inspector’s findings as documentation. Sellers take written requests more seriously than verbal ones.

-

Understand what gets shared with the VA. The inspection report stays with you. However, if you request repairs that touch on health or safety issues, the VA appraiser may need to re-inspect those specific items before the loan closes. Plan for that extra step in your timeline.

-

Use the contingency if the deal goes bad. If the seller refuses to address serious defects, your inspection contingency lets you cancel and recover your earnest money. Do not let a seller’s resistance pressure you into closing on a property with known major problems.

Pro Tip: Use Jhunthomeinspections’ Create Request List™ tool to organize inspection findings into a clear, prioritized list your real estate agent can present directly to the seller. It cuts negotiation time and keeps communication clean.

Understanding what a licensed inspector covers helps you ask better questions during the inspection itself. Veterans who attend the inspection in person consistently report feeling more confident in their purchase decisions.

Key Takeaways

A home inspection is the only tool in a VA loan transaction that works entirely for the buyer, making it the most important optional step a veteran can take.

| Point | Details |

|---|---|

| Appraisal protects the lender | The VA appraisal checks market value and MPRs but does not work in the buyer’s interest. |

| Inspection uncovers what appraisals miss | Licensed inspectors access roofs, crawl spaces, and test all major systems. |

| Inspection costs are a protective investment | Paying $350–$600 upfront prevents repair surprises costing $5,000 or more. |

| Reports give negotiation power | Buyers can request repairs, credits, or cancel the deal using inspection findings. |

| Schedule inspection before appraisal | Early scheduling preserves negotiation time and protects earnest money. |

Why I think skipping the inspection is the costliest mistake veterans make

Veterans often come into the homebuying process trusting the VA system to protect them. That trust is well-placed in many areas. But the VA appraisal is not one of them.

I have seen veterans walk into closing on homes with aging HVAC systems, deteriorated roofs, and electrical panels that needed full replacement. In every case, they assumed the appraisal had cleared the home. It had. The appraisal did exactly what it was designed to do: confirm the home’s value and basic habitability for the lender. It was never designed to protect the buyer.

The inspection contingency is one of the most powerful tools a buyer has, and veterans frequently waive it under competitive market pressure. That is a mistake I would never recommend. A seller who refuses to negotiate on serious defects is telling you something important about the deal. The inspection gives you the information to hear that message clearly.

Veterans deserve to enter homeownership with full knowledge of what they are buying. The $350–$600 inspection fee is not a cost. It is the price of certainty. And certainty, when you are making the largest purchase of your life, is worth every dollar.

— JOHN

Jhunthomeinspections: veteran-focused inspections in St. Louis and Southern Illinois

Veterans buying homes in the St. Louis Metro area and Southern Illinois have a specific ally in Jhunthomeinspections. The team specializes in serving first-time buyers, low-income families, and veterans navigating the VA loan process with confidence.

Jhunthomeinspections delivers thorough inspection services with comprehensive reports returned within 24 hours. The proprietary Create Request List™ tool helps you turn inspection findings into a clear repair request your agent can present to the seller immediately. Both in-person and video inspection options are available to fit your schedule. Transparent pricing and a pay-at-close option make the process accessible regardless of your budget. Book your inspection before the appraisal and give yourself the negotiating position you deserve.

FAQ

Is a home inspection required for a VA loan?

A home inspection is not required by the VA but is strongly recommended by industry professionals. Some lenders may require one as a condition of their loan approval.

What does a VA appraisal not cover?

The VA appraisal does not test mechanical systems, access crawl spaces, or climb roofs. It confirms market value and basic MPR compliance, leaving detailed system evaluations to a licensed home inspector.

How much does a home inspection cost for veterans?

Standard inspections cost $350–$600 and take 2–4 hours. Add-ons like termite, radon, and sewer scope testing cost $100–$300 each, depending on the property and region.

Can a veteran cancel a purchase based on inspection findings?

Yes. An inspection contingency in the purchase contract gives you the legal right to cancel the deal and recover your earnest money if inspection findings are unacceptable.

What programs help veterans with repairs after purchase?

Veterans may access cash-out refinance options and disability housing grants for post-purchase repairs. Some repair programs are specifically available to veterans and rural residents through federal agencies.

Recent Comments