A termite inspection for a VA loan, formally called a wood-destroying insect (WDI) inspection, is not required on every purchase. Whether your home needs one depends on the property’s location, the loan type, and what the VA appraiser observes during the appraisal visit. Veterans using purchase loans or cash-out refinances in designated risk areas will almost certainly face this requirement. Those using an Interest Rate Reduction Refinance Loan (IRRRL) typically will not. Understanding the termite inspection VA loan requirement before you reach the closing table protects both your loan approval timeline and your long-term investment.

How does the VA termite inspection requirement vary by state and county?

The VA does not mandate WDI inspections nationwide. Instead, the requirement is location-dependent, handled through a framework of local requirements that differ by state and sometimes by individual county. This is the single most misunderstood aspect of VA loan pest inspections, and the confusion costs buyers time and money every year.

The VA uses Termite Infestation Probability (TIP) zones to classify geographic risk. TIP zones range from moderate to heavy risk areas, where inspections are typically required, down to low-risk zones where they may not be. The U.S. Department of Agriculture developed these zones based on climate, soil conditions, and documented termite activity, so they reflect real biological risk rather than bureaucratic guesswork.

States fall into three broad categories when it comes to VA termite inspection requirements.

| Category | Description | Example States/Areas |

|---|---|---|

| Statewide requirement | WDI inspection required on all covered VA loan transactions | Alabama, Georgia, Florida, South Carolina |

| County-specific requirement | Inspection required only in designated counties | Parts of California, Virginia, Missouri |

| Appraiser-triggered only | No blanket requirement; inspection ordered if appraiser notes evidence | Most northern and mountain states |

The practical implication is significant. A veteran buying in Atlanta, Georgia faces a mandatory WDI inspection regardless of the home’s condition. A veteran buying in Minneapolis, Minnesota likely faces no requirement unless the appraiser spots visible damage or infestation signs during the walkthrough. Checking your specific county’s status with your lender before the appraisal is scheduled is the fastest way to know where you stand.

Pro Tip: Ask your VA-approved lender for the local requirements list specific to your county before the appraisal is ordered. This one step eliminates the most common source of last-minute closing surprises.

When and why is a WDI inspection needed during the VA loan process?

The VA appraisal and the WDI inspection serve different purposes, and separating them mentally helps you anticipate what is coming. The appraisal evaluates whether the property meets VA Minimum Property Requirements (MPRs) for safety, soundness, and sanitation. The WDI inspection is a specialized report that focuses exclusively on wood-destroying organisms and any structural damage they have caused.

Four specific triggers can make a WDI inspection part of your loan conditions:

- Geographic location. Your property sits in a state or county where the VA’s local requirements mandate a WDI report for all purchase or cash-out refinance transactions.

- Appraiser observation. The VA appraiser notices visible signs of infestation, wood damage, or conditions favorable to pests and notes them in the appraisal report, even in a low-risk state.

- Loan type. Purchase loans and cash-out refinances in covered locations require WDI reports. IRRRLs are exempt in every state.

- Lender overlay. Some lenders add their own requirements beyond VA minimums, so a lender may require a WDI report even when the VA does not.

Timing matters more than most buyers realize. The WDI inspection must be completed, reviewed, and any required treatments or repairs finished before the loan can close. Scheduling the inspection the week before your target closing date is a reliable way to push that date back by two to four weeks if problems are found. Treat the WDI inspection like the appraisal itself: schedule it as early as possible in the process.

Pro Tip: If you are buying in a county with a statewide requirement, schedule the WDI inspection the same week the appraisal is ordered. Running them in parallel rather than in sequence can save you two weeks or more.

What does the VA termite inspection process actually look like?

The WDI inspection is performed by a licensed pest control professional, not a general home inspector. The report follows the NPMA-33 form or a state-equivalent document, which is the industry-standard format recognized by VA lenders and underwriters. The scope of the inspection is broader than the name suggests.

A WDI inspection covers termites, carpenter ants, carpenter bees, and wood-boring beetles. The inspection is not termite-only, which means your budget and repair planning need to account for a wider range of potential findings. This distinction matters because carpenter ant damage, for example, can be structurally significant and expensive to remediate even though it receives far less public attention than termite damage.

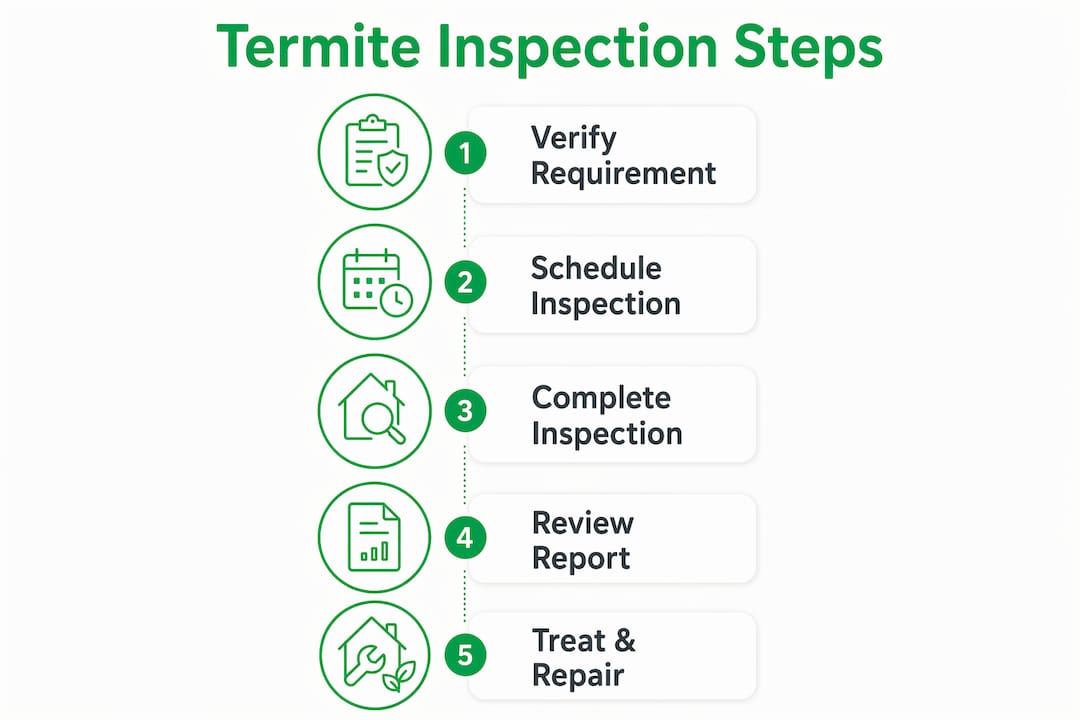

Here is what the full process looks like from start to finish:

| Step | Action | Who Is Responsible |

|---|---|---|

| 1. Confirm requirement | Verify local WDI requirement with lender | Buyer and lender |

| 2. Schedule inspection | Hire a licensed pest control professional | Buyer (or seller by negotiation) |

| 3. Inspection performed | Licensed inspector examines accessible wood structures | Licensed pest professional |

| 4. NPMA-33 report delivered | Report sent to lender and appraiser | Inspector |

| 5. Treatment and repairs | If infestation or damage found, licensed treatment and repairs completed | Seller (typically) or buyer |

| 6. Clearance inspection | Follow-up inspection confirms treatment success | Licensed pest professional |

| 7. Final report to lender | Clearance documentation satisfies underwriting condition | Inspector and buyer |

If the initial report comes back clean, the process ends at step four. If infestation or damage is found, treatment and repairs are required before the loan can close, and a second clearance inspection is often needed to confirm the work was completed correctly. The loan cannot close until all conditions tied to the WDI report are satisfied and documented in the underwriting file.

Pro Tip: Request the NPMA-33 report be sent directly to your lender the same day it is completed. Waiting for the report to travel through multiple hands adds days to your timeline for no reason.

Common mistakes veterans make with VA termite inspection requirements

The most expensive mistake is assuming the requirement applies universally. Many veterans believe all VA loans require a termite inspection, which leads to either unnecessary panic or, worse, the opposite error: assuming it does not apply to them when it does. Both assumptions cost money.

Here are the mistakes that most reliably delay VA loan closings or inflate costs:

- Waiting too long to schedule. Scheduling the WDI inspection after the appraisal report is returned adds unnecessary lag time. In states with statewide requirements, you already know you need it. Book it immediately.

- Ignoring minor damage findings. Past damage from wood-destroying insects, even if the infestation is no longer active, may still require repair under VA guidelines. Buyers who assume old damage is irrelevant often face surprise repair conditions from the underwriter.

- Misunderstanding cost responsibility. VA guidelines historically restricted buyers from paying for termite inspections in certain states, though this has evolved. Know your state’s current rules. In many transactions, the cost is negotiated as part of the purchase contract, and sellers often cover it. Failing to address this in the contract leaves the cost ambiguous.

- Failing to coordinate report delivery. The WDI report must reach the lender and be reviewed by the underwriter before closing can be scheduled. Buyers who assume the inspector handles this automatically sometimes discover the report was never forwarded.

- Overlooking the scope of WDI inspections. Because the inspection covers carpenter ants and beetles in addition to termites, repair costs can be higher than anticipated. Budget conservatively, not optimistically.

Reviewing home inspection requirements by loan type before you make an offer gives you a realistic picture of what you are committing to. Veterans buying in high-risk states who understand this process in advance are consistently better positioned to negotiate repair costs and keep closings on schedule.

Key takeaways

The VA termite inspection requirement is location-based and loan-type-specific, not universal, and understanding this distinction is the foundation of a smooth VA loan closing.

| Point | Details |

|---|---|

| Requirement is location-based | WDI inspections are required statewide in some states and only in specific counties in others. |

| Loan type determines applicability | Purchase loans and cash-out refinances may require WDI reports; IRRRLs are exempt in every state. |

| Scope exceeds termites | WDI inspections cover carpenter ants, beetles, and other wood-destroying insects, not just termites. |

| Timing is critical | Schedule the inspection early to allow time for treatment, repairs, and clearance before closing. |

| Findings must be resolved | If infestation or damage is found, treatment and a follow-up clearance inspection are required before loan approval. |

What I’ve learned from watching VA buyers navigate termite inspections

After working with veterans and first-time buyers through hundreds of transactions in the St. Louis Metro area and Southern Illinois, the pattern I see most often is not ignorance. It is overconfidence in secondhand information. A veteran hears from a friend that “VA loans always require termite inspections” or “VA loans never require them,” and they walk into the process with a fixed assumption that does not match their specific county’s rules.

My strongest recommendation is to verify the local requirement directly with your VA-approved lender before you make an offer, not after. This takes one phone call and eliminates the most common source of closing delays I have witnessed. The lender has access to the VA’s local requirements database and can tell you definitively whether a WDI report is required for the specific property address you are considering.

I also encourage buyers to treat the WDI inspection as a negotiating tool, not just a compliance checkbox. If the report comes back with findings, you have documented evidence of a structural issue that the seller is typically responsible for addressing. That is leverage. Buyers who understand why home inspections matter before they make an offer use inspection findings to their advantage rather than reacting to them with anxiety.

Budget for potential repairs regardless of who is contractually responsible. Sellers sometimes push back on repair costs, and having a realistic number in mind before negotiations start keeps the deal moving. A $500 termite treatment is not a deal-breaker. A buyer who is blindsided by it and has no financial cushion sometimes makes it one.

— JOHN

Get VA-compliant inspections from Jhunthomeinspections

Veterans and homebuyers in the St. Louis Metro area and Southern Illinois deserve inspections that keep their VA loan on track, not ones that create new complications.

Jhunthomeinspections provides thorough VA-compliant inspection services in St. Peters, University City, and surrounding communities, with comprehensive reports delivered within 24 hours. The team specializes in supporting veterans, first-time buyers, and low-income families through the home buying process, including coordinating WDI inspection documentation with lenders to prevent closing delays. If you need budget-friendly inspection options that still meet VA standards, Jhunthomeinspections has flexible solutions designed for buyers at every stage. Schedule your inspection early and give your closing timeline the room it needs.

FAQ

Does every VA loan require a termite inspection?

No. The VA requirement is location-dependent, applying statewide in some states and only in specific counties in others. IRRRLs are exempt from WDI inspection requirements in every state.

Who pays for the VA termite inspection?

Cost responsibility varies by state and is often negotiated in the purchase contract. In many transactions, the seller covers the inspection cost, but buyers should confirm local rules with their lender and address it explicitly in the contract.

What happens if the termite inspection finds damage?

If infestation or damage is found, treatment and repairs are required before the loan can close. A follow-up clearance inspection is typically needed to confirm the work was completed to VA standards.

Is a termite inspection the same as a home inspection for a VA loan?

No. The VA appraisal assesses Minimum Property Requirements for safety and soundness, while the WDI inspection is a specialized pest report focused on wood-destroying organisms. They serve different purposes and are performed by different professionals.

How do I know if my county requires a VA termite inspection?

Ask your VA-approved lender to check the VA’s local requirements for the specific property address. The lender has direct access to this information and can confirm the requirement before you schedule the appraisal.

Recent Comments